What Is Accrued Payroll?

Accrued payroll refers to the total amount of wages, salaries, and other employment-related costs that a business has accumulated but hasn’t yet paid by the end of an accounting period. You’ll find it listed as a current liability on the balance sheet. According to accrual accounting principles, it needs to be recognized in the period when the work was actually done, rather than when the payment is made.

How Accrued Payroll Works?

Accrued payroll comes into play because the dates when employees get paid and the end of accounting periods don’t usually match up. Employees earn their wages continuously, but they’re paid on a set schedule whether that’s monthly, bi-weekly, or weekly. So, when an accounting period wraps up before the next payday, the wages that have been earned since the last payment are still pending. According to accrual accounting, which is mandated by International Financial Reporting Standards (IFRS), US Generally Accepted Accounting Principles (GAAP), and Swiss GAAP FER, these unpaid amounts need to be recorded as an expense in the period they were earned, along with a corresponding liability on the balance sheet.

This requirement stems from the matching principle, a key concept in financial accounting. The matching principle dictates that expenses should be recognized in the same period as the revenue or activity they relate to, no matter when the cash actually changes hands. Accrued payroll is essentially the payroll version of this principle: the cost of labor done in March needs to be reflected in March’s accounts, even if the salaries aren’t paid out until April.

What Accrued Payroll Includes?

Accrued payroll goes beyond just unpaid wages; it includes all the compensation-related costs that have piled up during the accounting period but are still outstanding by the end of that period. Here are the key components to consider:

- Wages and salaries earned since the last payroll date: this is the total gross pay for all employees covering the days or hours worked from the last pay date up to the end of the period.

- Employer social insurance contributions: these are the payroll taxes and contributions that the employer is responsible for on the accrued wages, which include AHV/IV/EO, ALV, BVG, SUVA, and FAK in Switzerland.

- 13th month salary accrual: this represents one-twelfth of the annual entitlement for the 13th month, calculated for each month that has passed, and is recognized as a liability before the payment is made.

- Bonus and commission accruals: this includes any performance-related or contractual variable pay that has been earned during the current period but will be paid out later.

- Holiday and leave accruals: this refers to the monetary value of any unused leave entitlements that employees have earned but haven’t taken yet, which vest as they continue to work.

- Overtime accruals: these are the extra hours worked during the period for which payment hasn’t been processed yet.

The Accounting Entries

Accrued payroll is all about two key accounting events that happen around the payment date. At the end of the period, the employer acknowledges the expense and sets up a liability. Then, when it’s time to pay out the payroll, that liability gets cleared, and cash goes down. To avoid double-counting when the actual payroll is processed, many finance teams also make a reversal entry at the beginning of the new period.

When the period ends, the accrual entry hits the payroll expense on the income statement and credits the accrued payroll liability on the balance sheet. Later, when payroll is actually processed, the payment entry debits that liability and credits the bank account. And don’t forget the reversal entry, which is made on the first day of the new period to cancel out the accrual, ensuring that the full month’s payroll expense is only recognized once when the actual payroll runs.

Period-End Cut-Off

The accuracy of payroll that’s been accrued hinges entirely on how precisely the cut-off is applied at the end of each period. Cut-off refers to the process of determining which wages should be included in the current period and which should roll over to the next. For a company that pays salaries on the 25th of each month, with the period ending on the last day of the month, it’s crucial to accrue wages earned from the 26th to the 31st. This typically covers five or six calendar days of payroll costs, which can add up to a significant amount for a large Swiss employer. To ensure financial comparability across different reporting periods, it’s vital to consistently apply the same cut-off methodology from one period to the next.

Accrued Payroll Formulas and Journal Entries

The following formulas cover every calculation step required to determine the accrued payroll liability at any period end date. All monetary examples use Swiss franc figures and 2024 Swiss statutory contribution rates.

Core Accrual Formulas

| Formula 1: Daily Gross Pay Rate

Daily Gross Rate = Monthly Gross Payroll / Number of Calendar Days in the Month This rate is the foundation of the accrual calculation. It converts the monthly payroll cost into a per-day figure that can be multiplied by the number of days to accrue. Example: CHF 285,000 total monthly gross / 30 days = CHF 9,500 per calendar day. |

| Formula 2: Gross Wage Accrual

Gross Wage Accrual = Daily Gross Rate x Number of Days to Accrue Days to accrue = number of calendar days from the last payroll date to the period end date (inclusive). Example: last payroll date 25 March, period end 31 March = 6 days. CHF 9,500 x 6 = CHF 57,000 gross wage accrual. |

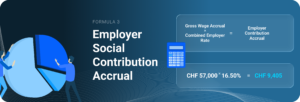

| Formula 3: Employer Social Contribution Accrual

Employer Contribution Accrual = Gross Wage Accrual x Combined Employer Rate Combined employer rate in Switzerland = AHV/IV/EO 5.30% + ALV 1.10% + BVG employer share (varies by age and fund) + FAK (canton-dependent) + SUVA/BU. A reasonable combined estimate for budgeting purposes is 16% to 20% of gross wages. Example: CHF 57,000 x 16.50% = CHF 9,405. |

| Formula 4: 13th Month Monthly Accrual

13th Month Monthly Accrual = Total Monthly Gross Payroll / 12 Accruing one-twelfth of the annual 13th month entitlement each month ensures the liability is spread evenly across the year. Example: CHF 285,000 / 12 = CHF 23,750 per month. For the 6-day period accrual: CHF 23,750 / 30 x 6 = CHF 4,750. |

| Formula 5: Holiday Leave Accrual

Holiday Accrual per Employee = (Annual Salary / 52 weeks) x Weeks of Leave Earned but Not Taken In Switzerland, employees are entitled to a minimum of four weeks paid leave per year (five weeks for employees under 20). The monetary value of unused leave must be recognised as a liability under IAS 19. Example: annual salary CHF 114,000 / 52 = CHF 2,192.31 per week. 1.5 weeks unused = CHF 3,288.46 accrual. |

| Formula 6: Bonus Accrual

Bonus Accrual = (Estimated Annual Bonus / 12) x Months Elapsed in Performance Period Where a bonus is probable and can be estimated reliably, it must be accrued in the period to which it relates. Example: estimated annual bonus CHF 12,000 / 12 = CHF 1,000 per month. After 9 months: CHF 1,000 x 9 = CHF 9,000 accrual. |

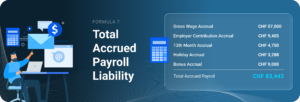

| Formula 7: Total Accrued Payroll Liability

Total Accrued Payroll = Gross Wage Accrual + Employer Contribution Accrual + 13th Month Accrual + Holiday Accrual + Bonus Accrual This is the total current liability that must appear on the balance sheet at period end. It represents the full cost of employment incurred but not yet settled in cash. All components should be calculated separately and documented in a supporting reconciliation schedule. |

Journal Entry Structure

The table below outlines the complete double-entry sequence for a Swiss employer managing a team of 30 people, each earning an average monthly salary of CHF 9,500, with payroll processed on the 25th of each month. As of March 31, 2024, the calculations reflect the accrual of 6 days’ wages, using the Swiss social contribution rates applicable for that year.

| Step | Account | Debit (CHF) | Credit (CHF) |

| STEP 1: 31 March period end: Recognise accrued payroll (6 days wages unpaid) | |||

| DR | Payroll Expense (P&L) | 47,500.00 | |

| CR | Accrued Payroll Liability (Balance Sheet) | 47,500.00 | |

| Basis: CHF 285,000 monthly gross / 30 days x 5 working days = CHF 47,500 | |||

| STEP 2: 31 March: Employer social contributions on accrued wages | |||

| DR | Payroll Expense Employer Contributions (P&L) | 7,837.50 | |

| CR | Accrued Social Contribution Liability (Balance Sheet) | 7,837.50 | |

| AHV/IV/EO 5.30% + ALV 1.10% + BVG est. 8.00% + FAK est. 2.10% = 16.50% x CHF 47,500 | |||

| STEP 3: 1 April: Reversal of period-end accrual (start of new period) | |||

| DR | Accrued Payroll Liability (Balance Sheet) | 47,500.00 | |

| CR | Payroll Expense (P&L) | 47,500.00 | |

| DR | Accrued Social Contribution Liability (Balance Sheet) | 7,837.50 | |

| CR | Payroll Expense Employer Contributions (P&L) | 7,837.50 | |

| STEP 4: 25 April: Actual payroll payment processed | |||

| DR | Payroll Expense (P&L) | 285,000.00 | |

| CR | Bank / Cash (Balance Sheet) | 285,000.00 | |

| Net effect: March expense = 6/30 x full month. April expense = 24/30 x full month. Total = 1 full month. | |||

Worked Accrual Calculation

The table below builds the full accrued payroll balance step by step for the same scenario, including gross wages, 13th month accrual, and employer social contributions.

| Scenario: 30-person team, CHF 9,500 avg monthly salary, 6 days accrued | Calculation (CHF) | Amount (CHF) |

| STEP 1: Gross Wage Accrual | ||

| Total monthly gross payroll (30 x CHF 9,500) | 30 x 9,500 | 285,000.00 |

| Daily gross rate (285,000 / 30 calendar days) | 285,000 / 30 | 9,500.00 |

| Days to accrue (26 March to 31 March = 6 days) | 9,500 x 6 | 57,000.00 |

| GROSS WAGE ACCRUAL | 57,000.00 | |

| STEP 2: 13th Month Monthly Accrual (1/12 per month) | ||

| Monthly 13th month accrual (285,000 / 12) | 285,000 / 12 | 23,750.00 |

| Pro-rated for 6-day accrual period | 23,750 / 30 x 6 | 4,750.00 |

| 13TH MONTH ACCRUAL (6-day period) | 4,750.00 | |

| STEP 3: Employer Social Contributions on Accrued Gross | ||

| AHV/IV/EO employer (5.30% x 61,750) | 61,750 x 5.30% | 3,272.75 |

| ALV employer (1.10% x 61,750) | 61,750 x 1.10% | 679.25 |

| BVG employer est. (8.00% on insured salary est.) | 61,750 x 8.00% | 4,940.00 |

| FAK family allowances est. (2.10%) | 61,750 x 2.10% | 1,296.75 |

| EMPLOYER CONTRIBUTION ACCRUAL | 10,188.75 | |

| TOTAL ACCRUED PAYROLL LIABILITY (Balance Sheet) | 57,000 + 4,750 + 10,188.75 | 71,938.75 |

Just a heads up, the BVG employer contribution is roughly estimated at 8% of the accrued gross amount for illustration. The actual BVG rates can vary based on the age distribution of employees, the specific pension fund in question, and whether the rate covers both savings and risk components. For the FAK rate, we’re using an estimate from the Canton of Zurich, which is 2.10%. Keep in mind that actual rates can differ from canton to canton.

Why Accrued Payroll Matters for Finance and HR Teams?

Accrued payroll is a significant item on the balance sheet, especially for businesses that rely heavily on labor. In the service sector, labor costs usually account for about 50% to 80% of total operating expenses. If there’s an error or omission in the accrual, it can lead to a serious misstatement in both the income statement and the balance sheet.

Financial Statement Accuracy and Audit Risk

If payroll accruals are left out or not accurately reported at the end of a period, it leads to an understatement of operating expenses on the income statement and current liabilities on the balance sheet, both by the same amount. This discrepancy can impact the reported operating profit, working capital ratios, and any financial covenants linked to these figures. External auditors often focus on payroll accruals as a high-risk area during their substantive procedures. If an accrual lacks a solid, documented calculation that aligns with the underlying payroll data, it can become a frequent issue in audits and might necessitate a restatement.

Cash Flow Forecasting

Accrued payroll is essentially a future cash outflow that we know will happen on a specific date. When finance teams keep a close eye on this liability, they can accurately predict how much cash they’ll need for payroll, helping to prevent any cash flow issues when payday rolls around. For companies dealing with payroll in multiple currencies, there’s an added layer to consider: if wages are recorded in one currency but the company reports in another, fluctuations in exchange rates between when the wages are accrued and when they’re actually paid can impact the cash cost. This is something that needs to be carefully managed as part of the treasury operations.

Swiss Regulatory Compliance

In Switzerland, when it comes time to submit the annual AHV salary declaration to the cantonal compensation office, it’s crucial that it aligns perfectly with the payroll records for the year. If there are any discrepancies between what’s been accrued and what’s actually been paid, and they aren’t clearly explained and documented, the compensation office might take a closer look during employer audits. According to the Swiss Code of Obligations, employers are required to keep payroll records for a decade, as stated in Article 958f, and those accrual schedules are an essential part of those records.

Accrued Payroll in Switzerland and Across Countries

The core accounting principle remains the same across all major frameworks. That said, the specific elements that need to be accrued, the standards that dictate how they’re measured, and how they interact with local payroll requirements can vary from one jurisdiction to another.

Switzerland

If you’re a Swiss company getting ready to prepare your financial statements under Swiss GAAP FER, IFRS, or the Swiss Code of Obligations, you’ll need to follow accrual accounting. This means that any wages that have been earned but not yet paid by the balance sheet date should be recorded as a current liability. Typically, the Swiss payroll accrual covers several key components: the gross wages that have accrued since the last payroll date; the employer’s share of AHV/IV/EO contributions (which is 5.30% of gross wages); ALV contributions (1.10% of gross, up to an annual ceiling of CHF 148,200); BVG occupational pension contributions (which vary by age and are determined by the pension fund); SUVA accident insurance premiums; FAK family allowance contributions (which vary by canton, usually between 1.5% and 3.0%); and the accrual for the 13th month salary (which is one-twelfth of the annual entitlement each month).

Additionally, Swiss companies also need to account for holiday entitlements under IAS 19 when applicable, or under Swiss GAAP FER as a provision for future obligations. According to Article 329a of the Code of Obligations, all employees are entitled to a minimum of four weeks of statutory leave, which means there’s an ongoing holiday accrual balance that must be kept up to date with current salary rates and reviewed at the end of each period.

| Country / Standard | Governing Framework | Key Components to Accrue | Holiday Accrual Required |

| Switzerland (Swiss GAAP FER) | Swiss GAAP FER / Code of Obligations | Gross wages, AHV/IV/EO, ALV, BVG, SUVA, FAK, 13th month | Yes, unused leave entitlement |

| Switzerland (IFRS) | IAS 19 Employee Benefits | All short-term benefits: wages, social charges, leave, bonus | Yes, under IAS 19 para 13 |

| Germany (HGB) | Handelsgesetzbuch | Wages, social contributions, provisions for holiday and bonus | Yes, as Rueckstellung (provision) |

| United Kingdom (FRS 102) | FRS 102 / IFRS | Wages, employer NICs (13.8%), accrued leave, bonus provisions | Yes |

| United States (US GAAP) | ASC conceptual framework | Wages, FICA (6.2% SS + 1.45% Medicare), accrued vacation (state rules) | State-dependent; mandatory in California |

| France (PCG) | Plan Comptable General | Wages, URSSAF contributions, paid leave provision (ICP) | Yes, provision for paid leave (CP) |

IAS 19 and Short-Term Employee Benefits

Under IAS 19 Employee Benefits, which is the IFRS standard that covers all employment costs, companies are required to recognize the total amount of short-term employee benefits that are expected to be paid for services rendered during a reporting period, without any discounting. These short-term benefits can include wages, salaries, paid annual leave, paid sick leave, profit-sharing, bonus plans, and even non-monetary perks. The good thing about IAS 19 is that it simplifies the measurement process by not allowing the discounting of these short-term obligations. For Swiss companies listed on the Swiss Exchange or those reporting to multinational parent companies under IFRS, IAS 19 serves as their main standard for accrued payroll.

Accrued Payroll vs. Payroll Expenses

These two terms refer to accounting concepts that are related yet distinct. They function at different stages of the reporting cycle and show up on separate financial statements. It’s quite common for people to mix them up, which can lead to mistakes during the period-end close.

| Feature | Accrued Payroll | Payroll Expenses |

| Definition | Earned but unpaid compensation recognised at period end | Total compensation cost recognised on the income statement |

| Financial statement | Balance sheet, under current liabilities | Income statement, under operating expenses |

| Timing | Point-in-time snapshot at period end cut-off | Cumulative flow of cost across the full reporting period |

| Nature | A liability: an obligation to pay in the future | An expense: the cost of labour consumed in the period |

| Reversal | Reversed when payroll is paid in the following period | Not reversed; represents permanent expense recognition |

| Components | Unpaid wages + employer contributions + 13th month + leave | All wages and contributions paid or accrued in the period |

| Audit focus | Completeness of cut-off; accuracy of rate assumptions | Occurrence, accuracy, and classification of all payroll costs |

| Switzerland example | CHF 57,000 of March wages unpaid at 31 March balance sheet date | Total payroll expense for the year including all paid wages and social contributions |

The relationship between these two elements can be summed up like this: Payroll Expense for a Period equals Cash Payroll Paid plus any increase in Accrued Payroll Liability (or minus a decrease). When the accrued payroll balance goes up from one period to the next, it means the recognized expense is greater than the cash paid. Conversely, if the balance goes down, the cash paid is more than the recognized expense. It’s essential for finance teams to reconcile these changes during the standard period-end close to ensure that the payroll expense on the income statement aligns with the liability on the balance sheet.

Best Practices for Managing Accrued Payroll

Document and Apply a Consistent Cut-Off Methodology

It’s crucial to clearly define how you measure the accrual period whether you’re using calendar days or working days, which payroll components are included, and how you calculate the daily rate. Make sure to document this methodology in your accounting policy manual and stick to it consistently each period. In Swiss payroll accounting, calendar-day accruals (where monthly payroll is divided by the total calendar days in the month) are the most widely used method, as they yield the most reliable results across months that have varying numbers of working days. If you switch up the methodology from one period to the next, it can lead to comparability issues and raise questions during audits.

Accrue All Components, Not Only Gross Wages

One of the most frequent mistakes in accruals is only calculating the gross wage while leaving out important elements like employer social insurance contributions, 13th month accruals, and leave provisions. In Switzerland, employer contributions can add around 16% to 20% on top of gross wages. If you skip these, you’re significantly underestimating both payroll expenses and current liabilities. To get it right, your complete accrual should encompass gross wages, all employer-side social contributions calculated at the relevant rates, the monthly 13th month installment, and any leave or bonus provisions that apply to the period.

Integrate Payroll and Finance Systems to Automate Journal Entries

Relying on manual accrual calculations in spreadsheets can lead to errors, take up too much time, and be tough to audit. By integrating your payroll platform with the general ledger, you can allow the payroll system to automatically send period-end accrual data straight into the accounting system. This generates compliant journal entries with the right account codes, amounts, and reversal dates. It cuts out the need for manual rekeying, speeds up the period-end close, and creates a clear audit trail from payroll data to financial statement balances, making it easy to review and approve without having to reconstruct everything manually.

Reconcile the Accrual to Payroll Data Every Period End

Before you post the accrued payroll balance to the general ledger, it’s essential to create a supporting reconciliation schedule. This schedule should detail the daily gross rate used, the number of days accrued, the accrual by payroll component, and a reference to the payroll register for that specific period. This reconciliation serves as the main evidence an auditor will look for when testing the accrual. Make sure it gets reviewed and signed off by the finance manager before you confirm the period close, and keep it as part of the statutory payroll record for the ten-year retention period mandated by Article 958f of the Swiss Code of Obligations.

Review Leave and Bonus Accruals Quarterly

Holiday leave entitlements and bonus provisions can shift throughout the year as employees earn leave, take time off, receive salary increases, and meet or miss performance targets. To keep your balance sheet accurate, it’s important to review and update these accrual balances quarterly. Use the current salary rates applied to any outstanding day balances and adjust your bonus probability estimates accordingly. An annual review at year-end just won’t cut it for businesses that need to provide interim financial reports or quarterly accounts for the board.

How Applic8 Handles Accrued Payroll?

Applic8’s As1 platform handles accrued payroll by automating the calculation, tracking, and reporting of provisions through its centralized, rule-based engine.

- Automatic Provisioning: The system allows for the automatic calculation of provisions by establishing specific rules that comply with the unique legal and entity-level requirements of each country.

- Standardization through GCT: Using the proprietary Global Compensation Tree (GCT), Applic8 creates a standardized framework that enables organizations to implement consistent automated calculations for various compensation and benefit accruals across all global locations.

- Streamlined Global Reporting: With a unified payroll database, managing and generating accurate global reports for “extra calculations like accruals” is “simple and straightforward”.

- Retroactive Accuracy: The platform natively handles automated retroactive calculations, ensuring that any past-period changes impacting accrual balances are adjusted correctly and automatically.

- Strategic Visibility: By moving accrual management out of manual spreadsheets and into an automated workflow, Applic8 eliminates “data chaos” and provides real-time visibility into these liabilities, transforming them into a strategic business asset.

Frequently Asked Questions About Accrued Payroll

How is accrued payroll calculated?

The basic formula is pretty straightforward: Daily Gross Rate equals Monthly Payroll divided by the number of calendar days in that month. To find the Gross Wage Accrual, you multiply the Daily Gross Rate by the number of days from the last payroll date up to the end of the period. Then, you calculate the employer’s social contributions on the accrued gross using the relevant statutory rates (in Switzerland, that includes AHV/IV/EO at 5.30%, ALV at 1.10%, the BVG employer share, FAK, and SUVA). Additionally, you add a 13th month accrual, which is one-twelfth of the annual entitlement, for each month. When you sum all these components, you get the total accrued payroll liability that gets posted to the balance sheet at the end of the period.

What’s the difference between accrued payroll and payroll expenses?

Payroll expenses show up on the income statement and reflect the total cost of employee compensation recognized during the period, whether it’s been paid out or accrued. On the other hand, accrued payroll is listed on the balance sheet as a current liability and only represents the part of that expense that hasn’t been paid in cash by the end of the period. When you settle the accrual in the next period, the liability gets reversed, cash decreases, but there’s no further impact on the income statement. The relationship can be summed up as: Payroll Expense equals Cash Paid plus the Change in Accrued Payroll Liability.

Does accrued payroll apply under Swiss GAAP?

Absolutely. Swiss companies that are preparing financial statements under Swiss GAAP FER, IFRS, or the Swiss Code of Obligations need to use accrual accounting. This means they must recognize wages that have been earned but not yet paid by the balance sheet date as a current liability. The accrual should cover gross wages, employer contributions for AHV/IV/EO, ALV, BVG pension, SUVA, FAK, and any accrued 13th month entitlement. Payroll platforms like As1 can help automate this calculation and create the necessary reconciliation schedule for audits, ensuring

Is holiday pay accrual required in Switzerland?

Absolutely! According to IAS 19 (for those following IFRS) and as outlined in Swiss GAAP FER, any unused annual leave that employees have earned but haven’t taken yet needs to be recognized as a liability. In Switzerland, employees are entitled to at least four weeks of paid leave each year, as stated in Article 329a of the Code of Obligations (and five weeks for those under 20). To calculate the accrual, you multiply the number of outstanding leave days by the employee’s daily salary rate on the balance sheet date, and this should be updated at the end of each period using the current rates.

How does accrued payroll affect the balance sheet?

Accrued payroll shows up as a current liability, usually listed under accrued liabilities or trade and other payables on the balance sheet. This increases total current liabilities and reduces net working capital by the same amount. For businesses that rely heavily on labor, this balance can be significant compared to total current liabilities and is closely examined by auditors, lenders, and investors who are looking at short-term financial commitments. When the accrual is paid in the next period, cash goes down, and the liability is cleared, leaving net working capital unchanged. The impact on the income statement happens during the accrual period, not when the payment is made.